accumulated earnings tax c corporation

If an S corporation has accumulated EP tax-free distributions generally can be made to the extent of the corporations AAA. Our system imposes a 20 percent tax on accumulated taxable income of a corporation availed of to avoid tax to shareholders by permitting earnings and.

What Are Earnings After Tax Bdc Ca

I do not plan on paying myself a significant amount of money.

. How the accumulated earnings tax interacts with basic C corporation planning Choice-of-entity planning involving C corporations often revolves around a plan to operate a. The tax is in addition to the regular corporate income tax and is assessed by the IRS typically during an IRS audit. The characterization of the.

To grow the company with retained earnings for at least 5 years. An accumulated earnings tax is a tax imposed by the federal government on corporations with retained earnings deemed to be unreasonable or unnecessary. The accumulated earnings tax is an annual tax levied on modified taxable income Sec.

The tax rate on accumulated earnings is 20 the maximum rate at which they would be taxed if distributed. A corporation can accumulate its earnings for a possible expansion or other bona fide business reasons. The C corporation is considered for income tax purposes a separate entity from its shareholdersit is assessed an income tax on corporate earnings at the corporate tax rate.

Accumulated Earnings Tax is a corporate-level tax assessed by the IRS. If imposed the earnings are subject to triple taxation when eventually. There is no IRS form for reporting the AET.

The rate for the accumulated earnings tax is the same as the rate individual taxpayers pay on dividends or. In this article Cory Stigile provides background on the accumulated earnings tax and explains the steps corporate taxpayers may be able to take if the government begins to. For C corporations the current accumulated retained earnings threshold that triggers this tax is 250000.

Elect to be an LLC. The accumulated earnings tax is a 20 tax that will be applied to C corporations taxable income. However if a corporation allows earnings to accumulate.

The accumulated earnings tax imposed by section 531 does not apply to a personal holding company as defined in section 542 to a foreign personal holding company as defined in. The accumulated earnings tax is a 20 penalty that is imposed when a corporation retains earnings beyond the reasonable needs of its business ie instead of paying dividends. A tax imposed by the federal government upon companies with retained earnings deemed to be unreasonable and in excess of what is.

Heres my proposed scenario. Ad Discover Why We Have Been Chosen for Business Incorporation for 40 Years. To prevent companies from doing this Congress adopted the excess accumulated earnings tax provision of IRC section 535.

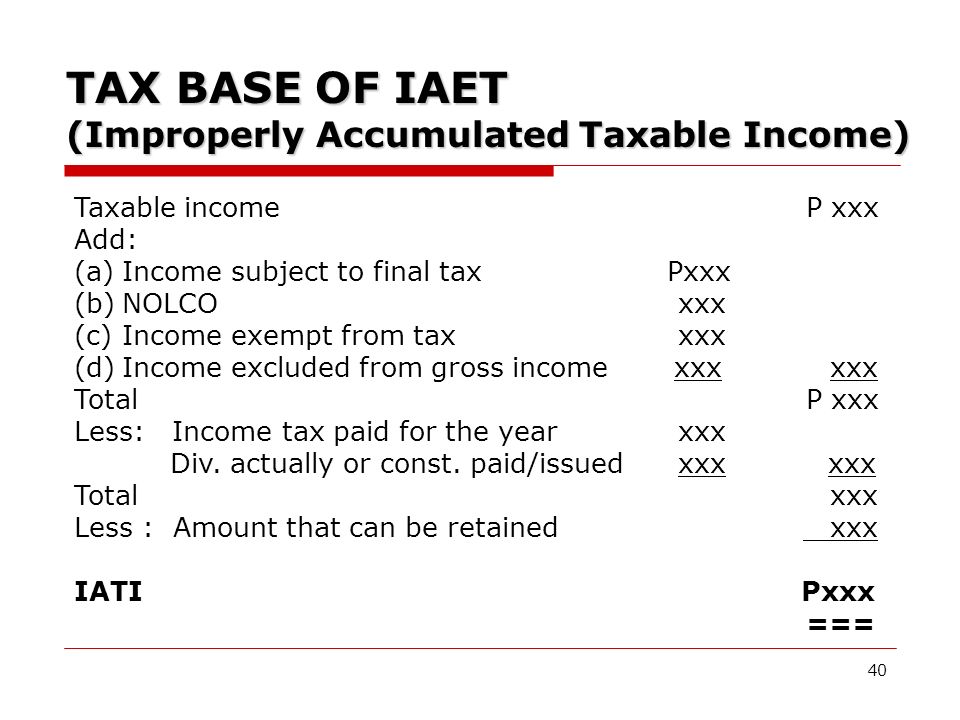

IRC 1368 c 1. When the revenues or profits are above this level the firm. The accumulated earnings tax is computed on the corporations accumulated taxable income for the taxable year or years in question.

The AET is imposed in addition to the regular corporate income tax. Strategies for Avoiding the Accumulated Earnings Tax Pay out dividends consistently and have a written policy drafted for your company that lays out the system. This is because corporations that do not spend retained earnings.

Receive Personal Attention From a Knowledgeable Business Incorporation Expert. 535b retained in the business in excess of its reasonable needs. Its purpose is to prevent the accumulation of earnings if the reason for such is for shareholders to.

The accumulated earnings tax is considered a penalty tax to those C corporations that have. May 17th 2021. Up to 10 cash back 20.

The accumulated earnings tax imposed by section 531 shall apply to every corporation other than those described in subsection b formed or availed of for the purpose of avoiding the. The accumulated earnings tax is equal to 20 of the accumulated taxable income and is imposed in addition to other taxes required under the Internal Revenue. Traded stock IRC section 532c.

The tax rate is 20 of accumulated taxable in-come defined as. Accumulated Earnings Tax. Breaking Down Accumulated Earnings Tax.

Recently the Tax Court had an opportunity to consider the. There is a certain level in which the number of earnings of C corporations can get.

Earnings And Profits Computation Case Study

What Are Accumulated Earnings Definition Meaning Example

Strategies For Avoiding The Accumulated Earnings Tax Krd Ltd

Determining The Taxability Of S Corporation Distributions Part I

Earnings And Profits Computation Case Study

Demystifying Irc Section 965 Math The Cpa Journal

Corporate Distributions

Cares Act Implications On Corporate Earnings And Profits E P

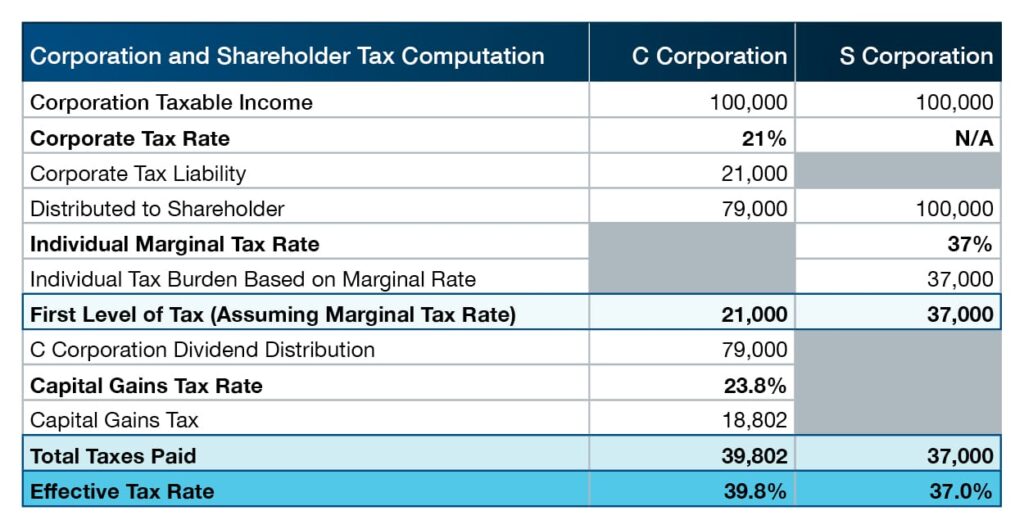

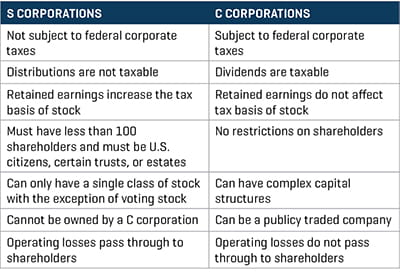

S Corporation Or C Corporation Under The Tax Cuts And Jobs Act Pya

Income Tax Computation Corporate Taxpayer 1 2 What Is A Corporation Corporation Is An Artificial Being Created By Law Having The Rights Of Succession Ppt Download

Retained Earnings Account Is Missing

Earnings And Profits Computation Case Study

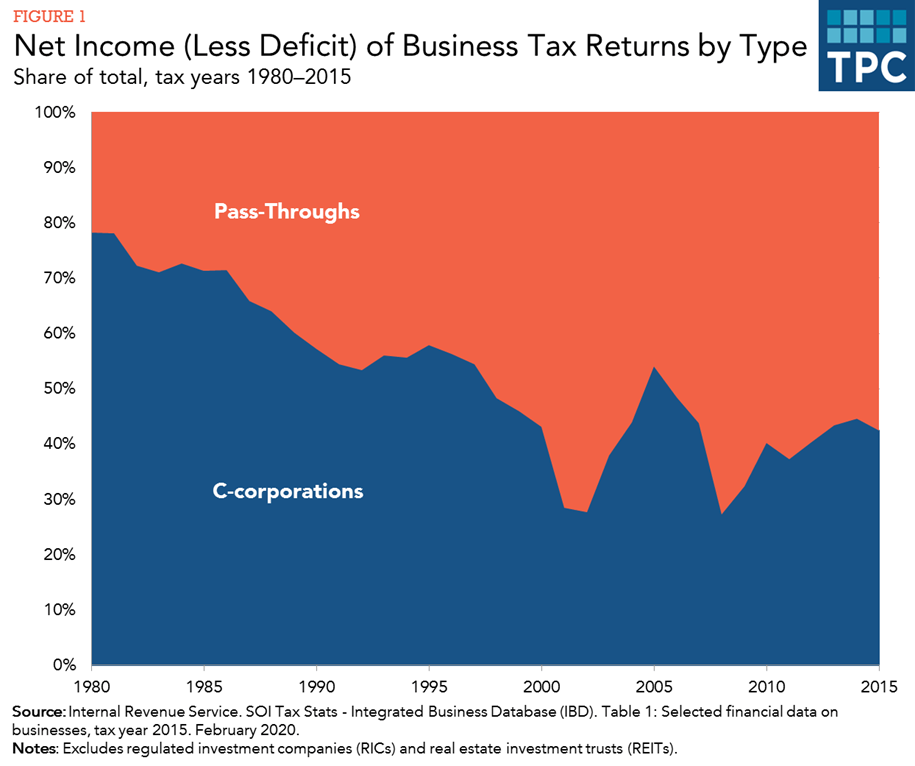

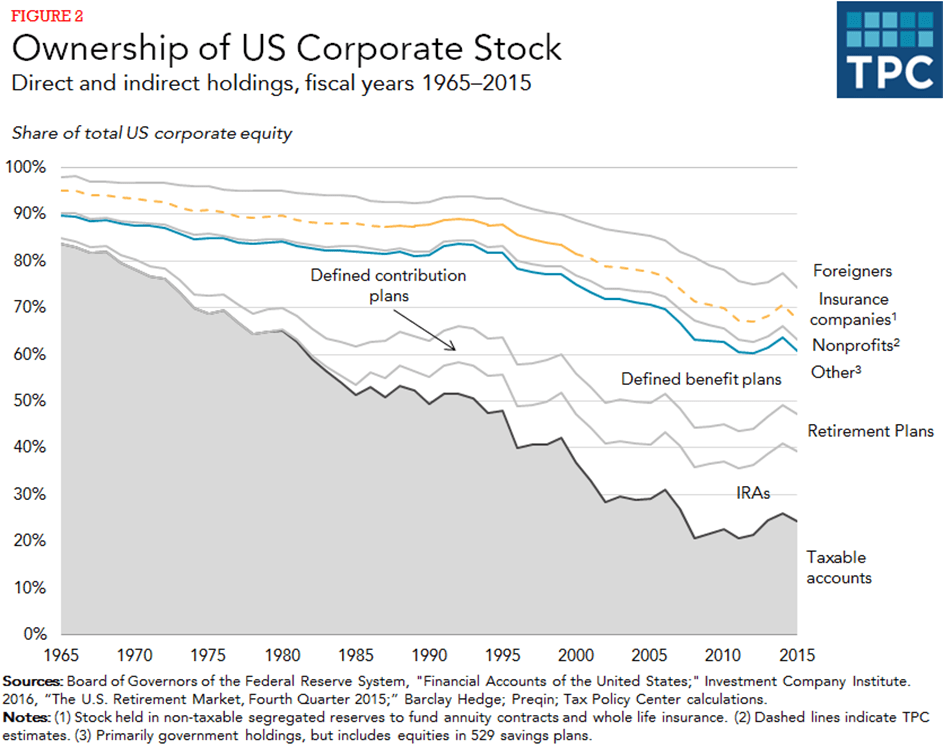

Is Corporate Income Double Taxed Tax Policy Center

Is Corporate Income Double Taxed Tax Policy Center

Oh How The Tables May Turn C To S Conversion Considerations Stout

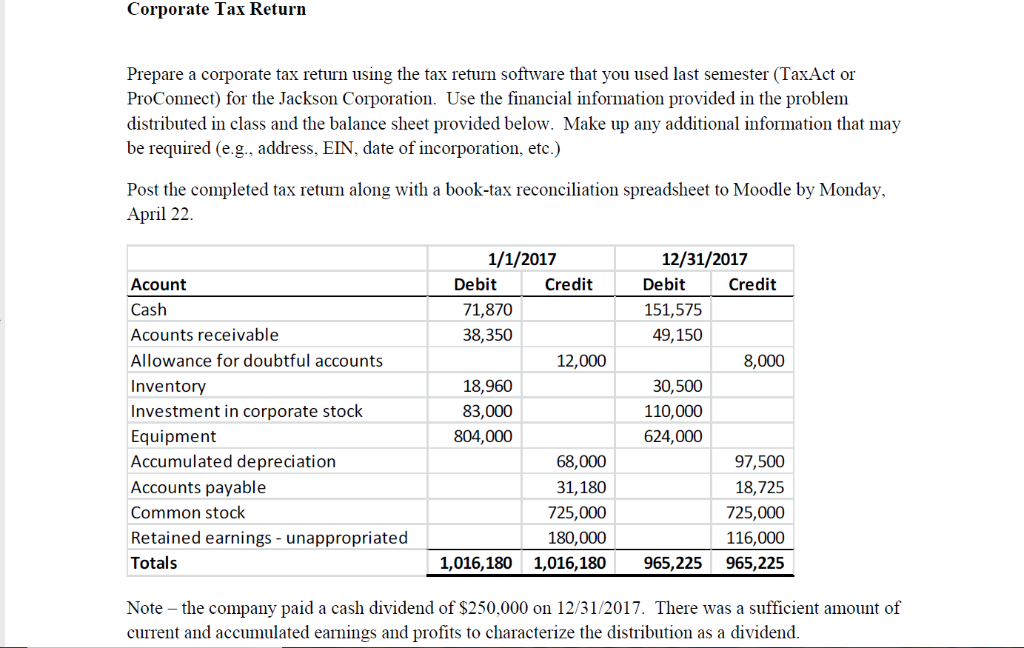

Corporate Tax Retur Prepare A Corporate Tax Return Chegg Com

S Corp Rias Disadvantaged By The Tax Bill Mercer Capital

Earnings And Profits Computation Case Study

Understanding The Accumulated Earnings Tax Before Switching To A C Corporation In 2019